In this week’s article, we explore the world of partnership draws and how entrepreneurs should approach paying themselves.

You are starting a business, congratulations! Now it is time to execute. Beyond your idea and business plan you are starting to face questions like how will I get paid? How do taxes work? Will my choices today impact my tax bill tomorrow? Is there anything I can do to reduce my tax liability? What is a partnership draw? What is a guaranteed payment? Should my company be an S-Corporation or a C-Corporation?

All of these are great questions and hopefully they have sparked your thinking. How you structure your startup from choice of entity to tax classification will drive how cash flows into and out of the business and the taxes associated with these activities. The following discussion skips the choice of entity decision process and assumes that your startup is a multi-member LLC, LLP, or other entity that will be taxed as a partnership. See our post about reasonable compensation to learn more about S-Corporations. C-Corporations are subject to double taxation but simplify investor taxes and are a preferred choice for many venture investors.

How will I get paid?

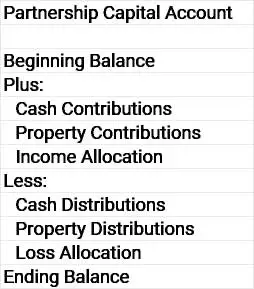

Your LLC or partnership interest capital account tracks your economic interest in your startup. A capital account is like a bank account, it goes up when you contribute cash or property and when you are allocated income. It goes down when cash or property is distributed to you and when losses are allocated. You are allowed to take a partnership draw also known as a cash distribution as long as your capital account balance (think bank account balance) is greater than zero. Note: this is a simplified example and there are other items that can impact this analysis like liability allocation and book capital vs tax capital.

The partners of the partnership decide how and when the they will take a partnership draw. This decision often considers available cash and future cash needs.

Tax law classifies partners in a partnership as self-employed and they should not be paid W-2 wages. See guaranteed payments below.

How do taxes work?

Each year the partnership issues a K-1 with your allocable share of the partnership’s income or loss. Your income or loss allocation is not necessarily related to the cash distributions you received during the year. This point is often big news to those not familiar with the tax concepts for flow-through entities like partnerships, S-Corporations, and certain trusts.

If you have been a wage earning employee in the past you know that any wages paid to you are reported on W-2 at the end of the year. Throughout the year your employer withheld income taxes and payroll taxes on your behalf and when you filed your taxes you may have received a small refund or owed some additional tax. The points to note here are you were only taxed on cash wages received and a large part of your taxes were prepaid throughout the year through withholding.

When you become a partner in a partnership your income allocation on K-1 is your share of the partnership’s income. You owe taxes on your share of partnership income and your capital account is adjusts by the same amount. A partnership draw also known as cash distribution reduces your capital account balance but does not impact taxes as long as your capital account maintains a positive balance. Your positive capital account balance might be thought of as previously taxed capital that can be distributed anytime tax-free. This can lead to timing differences in income recognition and cash in the hands of partners. Sometimes this mismatch is referred to as phantom income and should be planned for in advance.

Cash distributions do not impact taxes. You may owe tax on partnership income even if you did not receive cash!

With regard to tax payments generally partnerships do not withhold taxes on behalf of there partners. Partners make quarterly estimated tax payments or face an interest charge for failing to do so. Partnerships often withhold taxes on behalf of foreign partners.

What is my partnership income or loss allocation?

The answer is it depends. For simplicity let’s assume that there are three partners and profits and losses will be split equally. Further let’s assume that each contributed the same amount of cash to form the venture. In this case we allocate 33.3% of partnership taxable income to each partner. An example of a more complex allocation might be contributions that differ from sharing percentages or property contributed with a fair value greater than tax basis.

Startups should spend time discussing their business and the economic bargain between the partners with a CPA and attorney. The result of these discussions will be memorialized within a partnership or LLC operating agreement. The provisions of this agreement govern how cash will be distributed, how income and losses will be allocated, what happens if additional cash is needed for the business, and much more. Work these issues out in advance and you will avoid potentially significant issues in the future.

Discuss and come to an understanding with your partners. Then document within an operating agreement with the help of professionals who understand capital account maintenance and partnership tax provisions. An ounce of prevention is worth a pound a cure.

What is a guaranteed payment?

A guaranteed payment to a partner is similar to a salary to an employee and like a salary it is often a contractual obligation of the partnership to a partner for their time. An important distinction between a partnership draw and a guaranteed payment is a draw represents a share of profits. Profitability does not impact a guaranteed payment.

If the partners are a mix of founders and investors guaranteed payments may play a role in allocating cash compensation to founders first before profits or losses are allocated in accordance with the operating agreement.

Guaranteed payments may also play a role to equalize health insurance and other benefits for otherwise pro rata partners.

Tax implications follow guaranteed payments. Before you implement a guaranteed payment take time to understand the cash and allocation implications then clearly document within your operating agreement.

At Proseer we guide entrepreneurs and high net worth families through the intricacies of taxes and accounting. If you have questions about how to structure your startup, partnership draw, partnership allocations, guaranteed payments, or flow-through taxes contact us.