Cost Segregation Benefits for Real Estate Investors

If you own commercial real estate, you're already familiar with depreciation — the annual tax deduction that accounts for wear and tear on your building. But most investors don't realize they could be taking much larger deductions in the early years of ownership through a strategy called cost segregation.

With the One Big Beautiful Bill Act signed into law on July 4, 2025, 100% bonus depreciation has been permanently restored for qualifying property. That makes cost segregation more valuable today than it has been in years.

What Is a Cost Segregation Study?

A cost segregation study is an engineering-based analysis of your property that reclassifies certain building components into shorter depreciation categories. Instead of depreciating your entire building over 39 years (the IRS default for commercial property), a cost seg study identifies items that can be depreciated over 5, 7, or 15 years — and that now qualify for immediate 100% bonus depreciation.

Think of it this way: when you buy a commercial building, you're not just buying walls and a roof. You're also buying things like carpet, cabinetry, decorative lighting, parking lots, sidewalks, and landscaping. These items wear out faster than the building itself, and the tax code recognizes that by allowing them to be depreciated over shorter periods.

Common items reclassified in a cost seg study

5-year property (personal property): Carpet, decorative lighting, certain electrical and plumbing components, cabinetry, appliances, signage

15-year property (land improvements): Parking lots, sidewalks, landscaping, fencing, site drainage, exterior lighting

Why Does This Matter Right Now?

Under the One Big Beautiful Bill Act (OBBBA), any qualifying property acquired after January 19, 2025 is eligible for permanent 100% bonus depreciation. That means you can deduct the entire cost of reclassified 5-year and 15-year property in the first year you place it in service.

Before this law passed, bonus depreciation had been phasing down — 80% in 2023, 60% in 2024, and it was heading to zero by 2027. That phase-down is now permanently reversed for new acquisitions.

The Difference a Cost Seg Study Makes

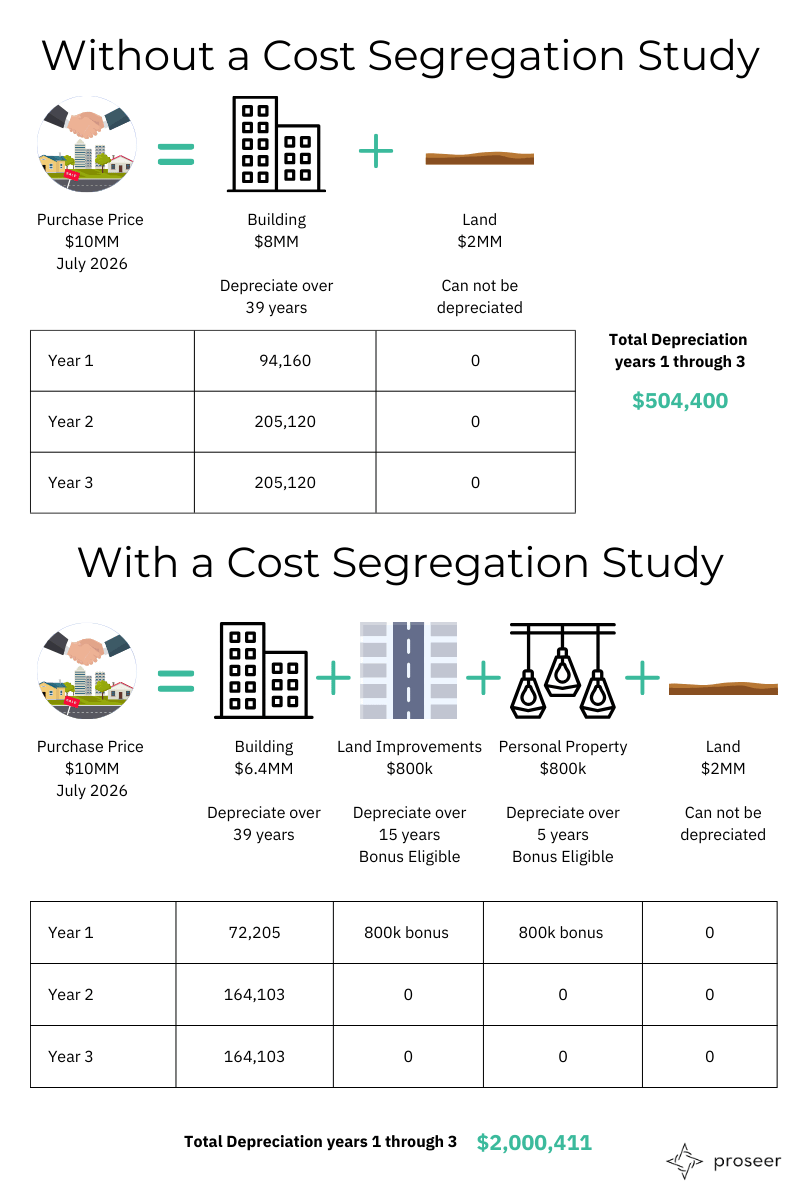

Let's look at a real-world example. Say you purchase a $10 million commercial building in July 2026, with $2 million allocated to land (which can't be depreciated).

Without a cost segregation study, you'd depreciate the $8 million building straight-line over 39 years. Your total depreciation over the first three years would be roughly $500,000.

With a cost segregation study, an engineer identifies $800,000 in personal property (5-year life) and $800,000 in land improvements (15-year life). Both categories qualify for 100% bonus depreciation. The remaining $6.4 million is still depreciated over 39 years. Your total depreciation over the first three years jumps to over $2 million — about four times more than without the study.

That accelerated depreciation translates directly into tax savings. At a 37% marginal tax rate, the difference could mean an additional $500,000+ in tax savings in the first three years alone.

Reclassification Estimates by Property Type

The percentage of your building's cost that can be reclassified into shorter depreciation categories varies by property type. Here are rough estimates based on typical cost segregation studies:

| Type of Structure | Reclassification Estimates |

|---|---|

| Apartments | 10% – 20% |

| Hotels | 20% – 30% |

| Office Buildings | 10% – 20% |

| Retail Stores | 15% – 25% |

| Grocery Stores | 20% – 30% |

| Manufacturing Facilities | 20% – 60% |

| Restaurants | 25% – 35% |

| Warehouses | 10% – 20% |

Manufacturing facilities tend to have the highest reclassification potential because they contain specialized equipment, heavy electrical systems, and process-specific infrastructure that qualifies for shorter depreciation lives.

Is a Cost Segregation Study Right for You?

Cost seg studies deliver the biggest benefits when:

Your property cost is at least $1 million — the savings need to outweigh the cost of the study (typically $5,000–$15,000 for most commercial properties).

You have taxable income to offset — the deductions are most valuable when you have income that would otherwise be taxed at high rates. Real estate professionals who materially participate can often use these deductions against active income.

You plan to hold the property for several years — while the tax savings are immediate, selling the property will trigger depreciation recapture, which is taxed at up to 25%. The longer you hold, the more you benefit from the time value of the upfront deductions.

You recently purchased, built, or renovated — a study can be done at any time, but the biggest benefit comes when paired with a recent acquisition or capital improvement.

When Cost Segregation May Not Be Worth It

Cost segregation isn't the right fit for every situation. The benefits can be significantly diminished — or even nonexistent — in certain circumstances.

If your rental activity is subject to passive activity rules and you don't have passive income to offset, the accelerated depreciation may simply create suspended losses that sit unused on your return. You'll eventually get the benefit when you sell or dispose of the property, but you lose the time-value advantage that makes cost seg so powerful in the first place.

Similarly, if the property is owned by foreign nationals or entities that can't fully utilize U.S. depreciation deductions, the study may not produce meaningful tax savings. And if you already have significant tax losses from other sources, generating additional depreciation may not move the needle.

The bottom line: cost segregation works best when the owner can actually use the deductions in the year they're generated. Before investing in a study, it's essential to evaluate your overall tax position — not just the property itself.

Important Things to Keep in Mind

Accelerated depreciation is a timing benefit, not free money. You're pulling future deductions into the present. When you eventually sell the property, the IRS will "recapture" the extra depreciation you took, taxing it at up to 25%. The real benefit is the time value of those early deductions — money saved today is worth more than money saved ten years from now.

The study must be done by a qualified professional. A proper cost segregation study involves an engineering analysis of the property, not just an accountant's estimate. The IRS has published an Audit Techniques Guide for Cost Segregation that outlines what a compliant study looks like. A well-documented study from a reputable firm will hold up under IRS scrutiny.

Don't let audit concerns hold you back. Some property owners hesitate because they worry a cost seg study could draw IRS attention. In practice, reputable cost segregation firms build their studies to meet IRS guidelines from the start — including detailed engineering reports, site visit documentation, and asset-by-asset classifications. A thorough, well-documented study is your best defense in the event of an audit, and the tax savings typically far outweigh the perceived risk.

You can do a "look-back" study on properties you already own. If you've owned a property for years and never had a cost seg study done, you can still benefit. The IRS allows you to claim the missed depreciation through a Form 3115 change in accounting method — no amended returns needed.

Next Steps

Cost segregation is one of the most powerful — and underused — tax strategies available to real estate investors. With 100% bonus depreciation now permanently available under the OBBBA, the window of opportunity is wide open.

Want to find out how much you could save?

Our team at Proseer can help you determine whether a cost segregation study makes sense for your property and connect you with qualified engineers to get it done.